Blockchain: applications beyond cryptocurrencies

3 February, 2022

By Cristina Pérez Solà & Víctor Garcia Font researchers of the IN3’s KISON group

In 2009, with the publication of the white paper Bitcoin: A Peer-to-Peer Electronic Cash System, an anonymous author, under the pseudonym Satoshi Nakamoto, proposed the operation of a new way of making digital payments, introducing a new monetary system managed and administered in a decentralized manner, the Bitcoin cryptocurrency. One of the main technological components proposed in this white paper is the blockchain, which, put simply, we could describe as a database that allows the transactions made with cryptocurrency to be stored in a distributed and traceable way.

Characteristics of cryptocurrencies

To understand what makes cryptocurrency special, we will first take a look at the characteristics of a conventional electronic payment system, such as a credit card. When paying by card, we need a large intermediary (such as a bank) to process the payment. We also delegate the responsibility for defining the monetary policy of the payment currency to the managers of a central bank, such as the European Central Bank in the case of payment in euros, or the Federal Reserve in the case of payment in US dollars. The main characteristic of cryptocurrencies such as Bitcoin is that there is no need for any of these banks (no intermediary to manage payments and no central bank) because these tasks are instead done collaboratively by the community of cryptocurrency users. This is why blockchain is said to create distributed and decentralized systems. These features give cryptocurrencies interesting properties, such as a high level of security and the elimination of single points of failure (there are thousands of computers offering the service around the world, meaning that the service does not depend on a few servers being operational), resistance to censorship (since there are so many service operators, it is difficult for a government to censor it), and a high level of traceability (each transaction is publicly recorded).

But a lot of time has passed since 2009 and the cutting-edge nature of blockchain technology has led to many more applications of this technology being proposed in addition to payment systems. It might seem contradictory but the objective of most cryptocurrencies is not to function as a global payment system, which is what Bitcoin aims to do, and they actually have other objectives. In fact, there has been so much evolution and popularization of this technology that the most popular websites, such as CoinMarketCap, have already indexed more than 16,000 cryptocurrencies for different purposes. For example, the second-largest cryptocurrency in market capitalization, Ether or ETH, is intended to be the exchange currency for running computer programs called smart contracts on the Ethereum blockchain platform. Thus, although we could potentially use ethers as a means of payment in a shop, they have a different purpose.

The popularization of decentralized applications

In fact, the Ethereum platform and smart contracts are bringing us a lot of the new applications in the blockchain world. The unique feature of these smart contracts is that a developer can set an arbitrary logic for an application and deploy it on a decentralized system such as Ethereum. Once deployed, the application becomes available to the entire community and acquires properties similar to those discussed above for cryptocurrencies (resistance to censorship, traceability, etc.). These applications are known as decentralized applications or DApps.

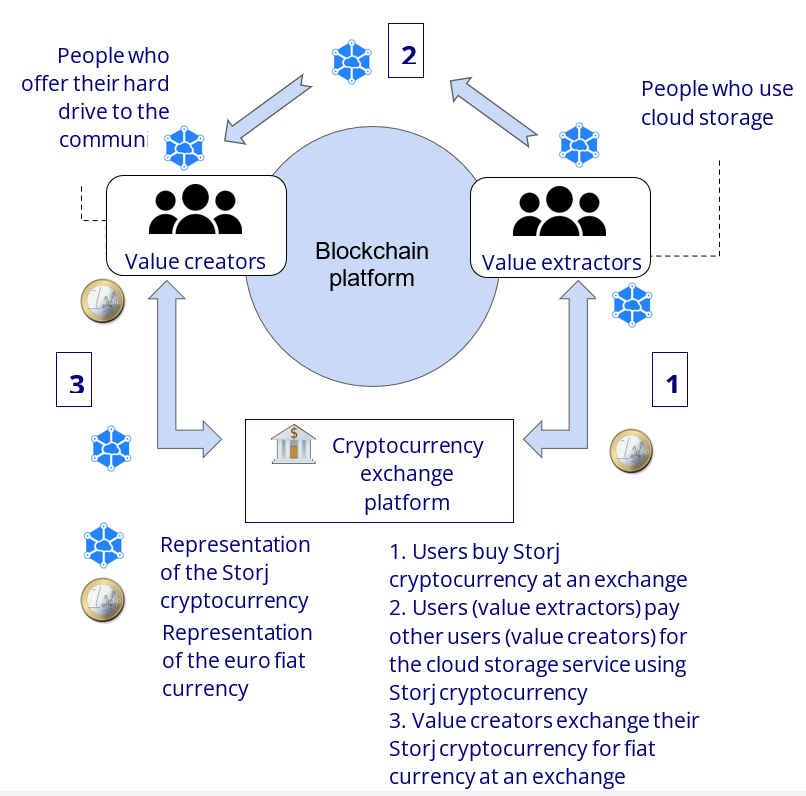

Once we have developed a way to create and deploy DApps, which can have any logic imaginable, it is a matter of letting our imagination run wild and starting to propose DApps to decentralize traditional, strongly centralized services. So, for example, there are proposals such as Golem, for building a network that acts as a supercomputer by adding the computing capacity of thousands of small users, or Storj, to create a decentralized cloud storage service that can compete with industry giants such as Dropbox. Most of these decentralized services aim to create a circular economic system based on a cryptocurrency where there are, on the one hand, value-extracting users, who are willing to purchase the cryptocurrency and use it to pay for a service (for example, storing data in the cloud on Storj), and on the other hand, value-creating users, who are willing to receive the cryptocurrency in exchange for offering a service (for example, offering their hard drives to store third-party data). If the cryptocurrency has enough liquidity, value creators will be able to exchange the received cryptocurrencies for conventional fiat currency, such as the euro.

In recent months, some of the DApps that have gained the most popularity are the set of decentralized finance services, also called DeFi. One of the most ambitious promises heard in the cryptocurrency world from the start is that cryptocurrencies would make it possible to build a more inclusive financial system. We know that the traditional system excludes millions of people in the world who cannot have a bank account because this would not be good enough business for the banks. Suddenly, with Bitcoin, we saw that anyone can create a Bitcoin wallet for themselves, without having to ask anyone’s permission, and thus start carrying out transactions with a digital payment system and offer their services to the whole world. DeFi DApps are now going a step further and allow, among other things, access to decentralized lending, insurance or currency exchange services, where the users themselves are the ones who end up offering the service through a traceable and open DApp, which acts as an intermediary. So, for example, any cryptocurrency holder can become a liquidity provider in exchange for interest. However, these applications are a double-edged sword. On the one hand, they don’t ask any questions about religion, income, or skin colour. On the other, nobody prevents users who have no technological or financial knowledge from losing their money through transactions that are too risky or don’t make sense.

As mentioned previously, one of the most noteworthy properties of blockchains is that they are highly traceable systems. As a result, many proposals have been made to use these systems in the world of logistics and for the creation of property records for different types of assets. In logistics, one of the most noteworthy projects is TradeLens, where Maersk and IBM are developing a system to record all the movements that goods make in global supply chains. As such, the aim is for the different participants in the chain (carriers, shipping companies, customs agents, etc.) to record and digitally sign in the blockchain for any operation they carry out. Thus, a transparent system would be achieved that would allow more efficient, global, and paperless control of the operations involved in the transportation of goods.

NFT fever

In terms of assets, one of the words that has gained popularity lately is NFT (non-fungible token). NFTs are digital assets that work like cryptocurrencies, but are conceptually more similar to collectible trading cards than to currencies such as the euro. When we have euros or bitcoins, what matters to us is the exact amount we have. So we might have 123 euros in our wallet (or 123 bitcoins in our cryptocurrency wallet) and, as holders, we aren’t interested in the serial number of the banknotes, but only that they are valid and allow us to purchase goods or services. In contrast, NFTs are digital assets that are exchanged like cryptocurrencies, but in which each asset uniquely represents something different. For example, we can have an NFT that represents a football star’s trading card, a digital work of art, or even a digital representation of a physical object. An example of the latter is Nike’s patent for trainers called CryptoKicks. The idea behind this system is for buyers to get an NFT that represents their shoes at the time of purchase (whether buying new or second-hand). Given that the second-hand market for trainers is enormous, this will allow the seller to display and transfer the NFT created by Nike to the buyer and thus cryptographically prove that the merchandise is not stolen or counterfeit.

The challenges of blockchain technology

So far, we have provided a good overview of many of the applications that blockchain technology can have. However, we have overlooked one rather obvious application and the reason why, in fact, this technology was originally proposed: payment systems. Although bitcoins and other cryptocurrencies are systems that have been in operation for several years, it is still difficult to find physical and electronic shops that accept these cryptocurrencies in exchange for their products. This is partly due to the slowness of payment confirmation and the possible fees that might have to be paid in order to carry out transactions efficiently. The payment speed depends on the level of risk we are willing to take on: even though the payments themselves can be considered immediate, we will have to wait for the network to confirm them if we want to make sure they have been carried out correctly. For example, a Bitcoin payment is considered to have been confirmed, on average, after one hour. It is clear that this waiting time, which may be suitable for some scenarios, is a problem when using cryptocurrency in physical shops! On the other hand, although fees are not mandatory, it is true that they are often necessary to get the network to validate the payment within the expected time. The fees paid to perform transactions with cryptocurrencies vary greatly: for example, in 2021, the average daily Bitcoin transaction fee ranged from just over €1 at the end of the year to over €60 in mid-April. And of course, once again, these amounts might be suitable for some situations (for example, when sending millions to the other side of the world or buying a car), but they are impractical when paying for a morning coffee or bus ticket.

To make up for these limitations and also solve other problems with the original cryptocurrency designs in the process, such as lack of scalability or privacy issues, Payment Channel Networks (PCNs) have been designed. They are a set of protocols that operate on top of blockchain-based cryptocurrencies and allow users to perform transactions quickly and much more cheaply. PCNs are therefore layer 2 protocols, working on top of a cryptocurrency, which they use as layer 1. The first PCN to be developed was the Lightning Network: the first draft of its design was published in 2015 and it was activated on the Bitcoin mainnet in 2018. The main idea of PCNs is to avoid the need for all transactions to be stored on the blockchain, thus overcoming the limitations that it introduced.

Thus, in the 13 years that have gone by since the creation of the blockchain-based cryptocurrency concept, this technology has already evolved enormously. Beyond offering a payment system that is secure and managed in a fully decentralized manner (which in itself is a huge contribution), blockchain technology offers the opportunity to decentralize (and eliminate the need to rely on third parties) many other use cases. This gives rise, as we have seen, to decentralized versions of financial products (products that are, traditionally, heavily controlled and regulated by various bodies), unique product representations (often subject to counterfeiting) through NFTs, and shared storage proposals (services usually provided by large corporations). Who dares to imagine where blockchain technology will lead us over the next decade?